Insurance for dummies

A primer on health insurance basics

Let’s get one thing straight.

The American healthcare system is messy.

It’s expensive for patients. It’s stressful for healthcare professionals.

And even though America spends $4T+ (17% of GDP) on healthcare alone, no one seems to understand how the system fully works.

Ourselves included! (we’re the dummies in the title)

Which is why we’ve decided to dig in and learn how healthcare works.

And we’re sharing our learnings along the way, starting with the basics of insurance.

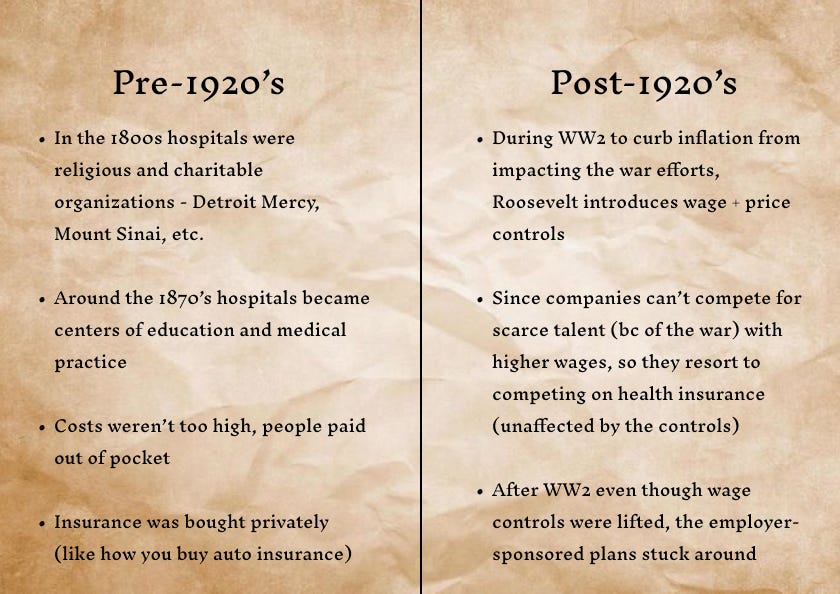

A small history lesson

Today, insurance in America is mostly dependent on your employment status.

If you have an employer → you have health benefits

If you’re unemployed → 😬

But it wasn’t always this way (you can thank Teddy Roosevelt for that).

Employer-based insurance is a big driver of healthcare costs.

Different employers choose to go with different health plans, which then leads to healthcare providers having to deal with different plans to get reimbursed, which leads to more admin costs for dealing with all the insurance plans.

There is a solution to this (having universal healthcare), but that’s a topic for another time.

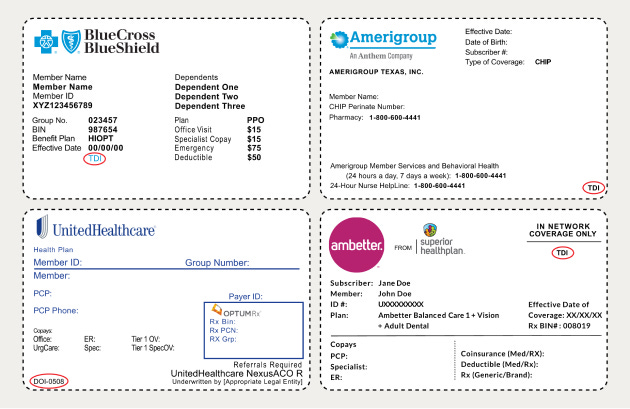

Health Plans 101

Most of us have a plastic card that resembles something like the ones in the picture above.

Few of us know what everything on the card means.

That’s what we’ll cover here.

What is a insurance health plan?

An insurance health plan is mainly a contract between an individual/employer and the insurance company outlining the covered services and how costs are handled.

FYI, health plan, insurance health plan, and insurance are interchangeable terms.

What are the different parts of a health plan you should know about?

Premium → The monthly amount you pay the insurance company for coverage

Copayment → The fixed amount you pay per visit

Coinsurance → The percentage of the total cost that you have to cover vs. the insurance company will cover

Deductible → The amount a patient has to cover before insurance starts covering expenses

i.e. If your plan has $5000 deductible this means you have to cover $5000 in medical expenses before the insurance company starts covering expenses

Embedded deductible - If you’re on a family plan you often have a smaller individual deductible as well as a larger family deductible

Individual deductible - Once an individual on a family plan meets their deductible, insurance will start covering expenses

Family deductible - once the whole family in aggregate meets their deductible (an amount set for the whole family), insurance will start covering expenses

Out of pocket max → the max amount you have to pay out of pocket (deductible + copay + coinsurance) until insurance will cover all remaining expenses

Copays do not count towards out of pocket max, you always have to pay copay

Coverage → Providers are either In-network (IN) or Out-of-network (OON) w/ your health plan

IN = healthcare provider and insurance company have a contractual agreement to provide services at pre-negotiated prices

OON = healthcare provider and insurance company don’t have a contractual agreement to provider services at pre-negotiated prices

What are the different types of health insurance plans (based on who provides it)?

Broad categories based on who provides the insurance

Government-sponsored health insurance → Health coverage programs funded and administered by the government.

Individual Health Insurances

Either bought directly by an individual from an insurance company or through the Health Insurance exchanges enabled by the Affordable Care Act (ACA)

Health Insurance exchanges are platforms for individuals and businesses to compare and purchase insurance (before you’d have to go to each insurance company directly)

Employer-sponsored insurance plans

These fall into two categories → fully-insured or self-funded

Fully-insured = employer pays fixed premiums to an insurance carrier, which assumes the financial risk for paying healthcare claims

Self-funded = employer assumes the financial risk for providing healthcare benefits to its employees

Usually larger companies opt for self-funded because it’s cheaper and more customizable. Self-funded is cheaper because

There are no state taxes on self-funded plans

You pay claims as they’re processed (so if the cost is less than the premium you save money)

Cuts out the admin costs you incur by using a carrier

A new wave of companies like Yuzu are helping SMBs launch self-funded plans as well → Less than a 1/3 of small businesses offer health benefits

Halle Tecco has written more about this here.

Short-term health insurance

Like the name suggests it’s for short terms (typically 12 months and up to 36 months

Health Care Sharing ministries (these are wild)

Insurance plans where members of a religious group cover each other’s insurance claims

Most insurance today (i.e. the one you have) is employer sponsored and is one of these types of alphabet soup managed plans

HMO - Health Maintenance Org

The primary care physician (PCP) acts as a gatekeeper and coordinates all care for the patient (provides referrals to specialists and other healthcare services)

Without a referral, the plan won’t cover the specialist care

No deductible

No OON Coverage

PPO - Preferred Provider Org

Has IN vs OON cost structures (OON is more expensive)

Has deductible

Has PCP copay & specialist copay

POS - Point of Service Plan

Same as an HMO plan, but has OON coverage

CDHP - Consumer Directed Health Plan

Good for healthier individuals who are less likely to use insurance

Higher deductibles, but lower monthly premiums

Paired w/ a tax-advantaged account such as Health Savings Account (HSA)/Health Reimbursement Arrangement (HRA)

HSA = An HSA is a tax-advantaged savings account that individuals can use to pay for qualified medical expenses. Contributions to an HSA are tax-deductible, and withdrawals for eligible expenses are tax-free. HSAs are also portable, meaning you can take the funds with you even if you switch employers.

HRA = An HRA is an employer-funded account that reimburses employees for qualified medical expenses. Unlike HSAs, HRAs are not portable and are typically tied to the employer.

The Insurance Business

Behind that plastic card are some very powerful people and companies.

Here are some you should know about. In future posts we’ll go more in depth about the inner workings of them (especially PBMs).

Insurers - provide insurance coverage, manage risk, and process claims

Ex. UnitedHealthcare (~$450B (as of 06/10/24) Minnesotan behemoth, larger than next 5 competitors combined), Blue Cross Blue Shield, Aetna, Cigna

Employers - offer health insurance as part of employee benefits packages, often sharing the cost of premiums with employees

Usually businesses or the government (if you’re in the public sector)

Third-Party Administrators (TPAs) - handle admin functions for self-funded plans (claims processing, provider network management, and customer service)

Ex. Meritain Health, UMR, HealthSCOPE Benefits

United Healthcare owns both UMR and HealthSCOPE, and you’ll see this pattern with a lot of health plan companies. They don’t want to lose money from employers choosing self-funded plans, so they’ll try to provide services that help with this.

Healthcare Providers - the people/institutions providing care (doctors, hospitals, clinics, specialists, pharmacies, etc.)

Government agencies - handle regulation and ensure compliance, provide public health insurance programs

Ex. Centers for Medicare & Medicaid Services (CMS), state insurance departments, the Department of Health and Human Services (HHS)

Brokers and agents - will help individuals or employers figure out what plan to buy

Can be independent (not tied to a specific insurance company) or captive (exactly as it sounds)

Pharmacy Benefit Managers (PBMs) - manage prescription drug benefits on behalf of health insurers, negotiate with drug manufacturers, process prescription drug claims

Stay tuned for a hit piece on PBMs by yours truly

Reinsurers - provide insurance to insurance companies, helping them manage risk by covering large or catastrophic claims

Ex. Munich Re, Swiss Re, Hannover Re

If you’ve gotten this far, congrats!

You’re no a longer a complete dummy when it comes to insurance.

In our coming posts we’ll cover what actually happens when you use your insurance card (Spoiler alert: the businesses above make money).

And if there’s anything in this primer you were curious about or think we should modify/add let us know!