The Meds Mafia

How drug pricing in America works

Imagine you're at the pharmacy counter, staring at a $300 price tag for your monthly medication. Now what if we told you that same drug actually costs $30 to make.

You may be asking, “Where's that extra $270 going?”

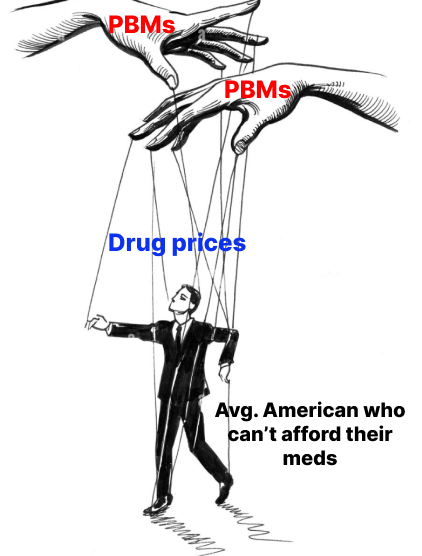

The answer: pharmacy benefit managers (PBMs) - the healthcare mafia you’ve never heard of.

In this post we’re going to pull back the curtain on how drug pricing in America works and the puppet masters pulling the strings (and lining up their pockets).

The Basics: Drug Pricing 101

Drugs fall into two categories - the 'formulary' list, which includes medications your insurance company might actually help pay for, and the 'non-formulary' list – over-the-counter meds, reproductive treatments, and cosmetic drugs not covered by insurance.

The formulary list is the one worth taking a closer look at (as is everything handled by insurance).

Imagine the drugs on the list as a fancy airline.

You've got your first-class drugs, your economy drugs, and everything in between. The specific tiers look like this:

Tier 1: Generics - The Economy Class

These are your generic drugs. They're like the basic economy seats – no frills, but they get the job done.

Cost: Around $10 for a month's supply.

These are equivalent to brand-name drugs but without the brand label price tag.

They don’t have to make up for R&D and marketing costs the brand might’ve incurred. → Generics are usually developed after a drug’s patent expires

Tier 2: Preferred brand - The Premium Economy

"Preferred brand" is like getting extra legroom, but for your medicine cabinet.

Cost: About $30 per month.

These drugs are "preferred" by your insurance company/PBM

The PBM has cut a deal w/ the manufacturer to then list their drug as the preferred (more on how this works later)

Tier 3: Non-preferred brand - The Business Class

Here we have the "non-preferred brand" drugs. You're paying for that brand name that the PBM doesn’t like!

Cost: Approximately $60 per month.

Tier 4: Specialty pharmacy - The Private Jet

Welcome to "specialty pharmacy" – think injectable drugs, cancer treatments, etc.

Cost: $1000+ per month.

These pricing dynamics are decided by a complex dance between pharmaceutical companies, insurance providers, and our shadowy mafia men - the PBMs.

Enter the PBM: The Wizard Behind the Curtain

The simplest description of PBMs is they’re middlemen between insurance plans and pharmaceutical companies. What this looks like in practice has evolved over time.

When PBMs started in the 1960s, they came in to help insurance companies with the growing volumes of prescription drug claims. They also started negotiating drug prices to be as low as possible for insurance plans’ patients.

This is very different than the mafia picture we’ve portrayed of PBMs. But starting in the 1980’s certain legal proceedings put the PBM villain arc into motion:

2003 - Medicare Modernization Act says Medicare can’t negotiate drug prices for it’s patient population. Only PBMs can do this.

* This recently changed with the Inflation Reduction Act, which allowed Medicare to negotiate. Classic government fixing a problem they helped create*2000s - Consolidations of PBMs into insurance companies are considered legal.

Until 2018, there were “gag clauses”, preventing pharmacists from recommending drugs to customers causing PBMs to profit less

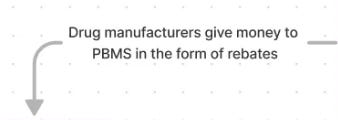

Before going into the details, here’s a quick diagram of the money flows:

If you haven’t spotted it already, the government precedents set in motion unlocked new revenue for PBMs. It’s this guy right here:

When you go from negotiating down prices with someone, and now get paid by that someone….

And this affects both pharmacies (who purchase the drugs from wholesalers) and patients.

But what does this mean? And more importantly how do PBMs/manufacturers get away with this?

The Infinite Money Glitch

PBMs have some unfair advantages enabling them to be massive monopolies.

We’ll cover the major ones - rebates, spread pricing, and consolidation.

Rebates

Earlier we mentioned how PBMs dictate which drugs go on to the formulary list, determining whether the drug is covered by their insurance partners. The higher up the drug is on the list, the more likely it is for the doctor to prescribe it (usually doesn’t require as much admin work).

And how does a manufacturer get their drug near the top of the list? By offering rebates.

The way rebates are supposed to work is they go to employers covering their employees’ insurance costs.

But what really happens is PBMs end up taking a large portion and giving the rest to employers. They get away with this because they’re not required to disclose any pricing negotiations/rebates.

So if the rebate was $100, they’ll take $75 and might tell the employer the rebate was only $25.

As a result, the rebates cause messed up incentives:

PBMs want to sell the higher cost drugs, because they can also get higher rebates on them

PBMs want more prescriptions bc they’ll make more money (rebates paid out more frequently)

Spread pricing

Spread pricing occurs when a PBM charges a health plan or employer more for a drug than it reimburses the pharmacy, and keeps the difference as profit.

Here’s a general example:

A patient is prescribed a 30-day supply of Generic Lisinopril (blood pressure medication).

Pharmacy Purchase - The pharmacy buys the drug from a wholesaler for $2.

Patient Purchase - A patient with insurance comes to fill their prescription. They pay their copay of $10.

PBM Reimbursement to Pharmacy - The PBM reimburses the pharmacy $20 for the drug. This covers the pharmacy's cost plus a small profit margin.

PBM Charges to Health Plan/Employer - The PBM then bills the health plan or employer $30 for this same prescription.

Spread Calculation Spread = Amount billed to health plan - Amount paid to pharmacy $30 - $20 = $10 → The PBM pockets this $10

This also happens because no one knows the true drug cost except for the PBM, not even the insurance companies that partner with PBMs!

Consolidation

As if rebates + spread pricing weren’t already a killer combo, the other advantage for PBMs is they’ve been rolled up into large insurance companies.

Three PBMs own two-thirds of the market, which has created an oligopoly:

Caremark (acquired for ~$21B) -> owned by CVS health (which has insurance company Aetna)

Express Scripts (acquired for ~$54B) -> owned by Cigna

OptumRx -> Owned by United Health

Each of these insurance companies have their hands in various parts of the money flow we charted out earlier. And now that they own PBMs, they have an incentive to do everything they can to grow their revenues.

At this point, the infinite money glitch may seem unstoppable, but luckily we have a well-known billionaire taking it on.

Enter the Maverick

In 2022, Mark Cuban started Cost Plus Drugs and used the infinity money glitch against PBMs.

Unlike PBMs with their secretive rebate schemes and pricing, Cost Plus Drugs operates on a transparent pricing model. Here's how it's tackling some of the industry's biggest issues:

Transparent Pricing: Cost Plus Drugs reveals its exact markup (15%) and pharmacy fee ($3) for each medication, eliminating the mystery of drug pricing.

No Rebates: By avoiding rebates altogether, the company removes the incentive for artificially inflated list prices.

Direct Negotiations: Cost Plus Drugs negotiates directly with drug manufacturers, cutting out layers of middlemen that typically drive up costs.

Consistent Pricing: All customers pay the same price for medications, regardless of insurance status, promoting equity in drug access.

Online Accessibility: As an online pharmacy (utilizing TruePill), it reduces overhead costs associated with traditional brick-and-mortar operations.

Focus on Generics: By emphasizing lower-cost generic medications, Cost Plus Drugs targets a segment of the market where traditional PBMs often extract significant profits.

While not a complete solution to all of pharma's pricing issues, Cost Plus Drugs is changing the industry. It's forcing traditional PBMs and pharmacies to reconsider their pricing models and bringing much-needed transparency to an opaque system.

As this model gains traction, it could lead to broader changes in how medications are priced and distributed in the United States. And even though this is a promising step in the right direction, there’s a lot of room for innovation!

If you’ve made it this far, we hope we’ve helped you understand the game of drug pricing!

We’re always looking to learn from others, so if you have any thoughts or building something in this space please feel free to reach out.

And if there’s anything you were curious about or think we should modify/add let us know!